A/B testing loan policies to optimise risk and business performance.

This project evaluates how different lending strategies impact default risk and profitability. By comparing a conservative and a growth-oriented policy, the analysis highlights the trade-off between reducing credit losses and scaling loan approvals using statistical testing.

1.

Business Problem — What Was the Challenge?

A lending company wanted to evaluate alternative loan approval policies to better manage credit risk, while still maintaining profitability.

The core challenge was clear:

How can we reduce the number of defaulting loans without limiting business growth?

2.

Approach & Method — How It Was Solved

To address this, we first defined a clear evaluation metric:

Default rate among approved loans

(P(loan_is_bad = 1 | approved = 1))

This metric directly captures the company’s risk exposure, as losses only occur when a loan is both approved and subsequently defaults.

We then designed two alternative loan policies:

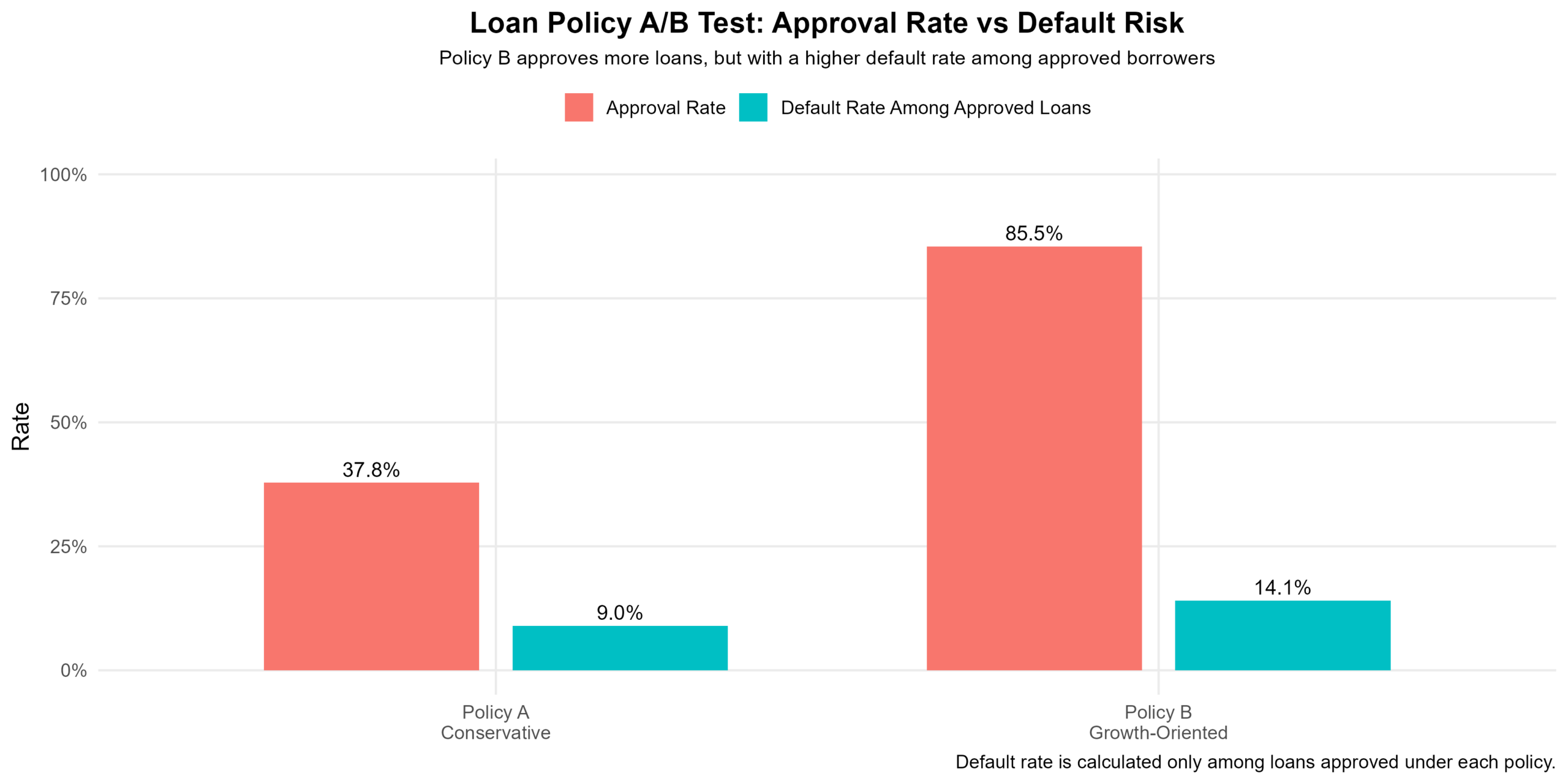

- Policy A (Conservative)

Stricter approval criteria → focuses on higher-quality borrowers - Policy B (Growth-Oriented)

More lenient criteria → increases loan approvals and market reach

Each policy was defined using key credit risk variables such as:

- loan grade

- debt-to-income ratio (DTI)

- annual income

Based on these thresholds, we determined which applicants would be approved under each policy.

To compare the two approaches, we conducted an A/B test, using a:

Two-proportion z-test

This allowed us to test whether Policy B leads to a significantly higher default rate compared to Policy A.

3.

Results & Business Insights

Policy B increases approvals significantly, but at the cost of a higher default rate among approved loans.

We tested the following hypotheses:

H₁: Policy B has a higher default rate than Policy A

H₀: No difference in default rates between Policy A and Policy B

Results:

- z = 17.65

- p < 0.001

The result is highly significant, meaning:

Policy B approves a significantly higher proportion of loans that default compared to Policy A.

What does this mean in practice?

- Default rate difference: +5.10 percentage points

- Equivalent to:

~51 additional defaults per 1,000 approved loans

Since each default represents a direct financial loss, this increase translates into substantially higher credit risk exposure.

Key Insight

- Policy A → Strong risk control

- Policy B → Higher growth, but higher risk

From a risk mitigation perspective, Policy A clearly outperforms.

4.

Business Implications and Limitations

While Policy A reduces default risk, it comes with an important trade-off:

Fewer approved loans → potentially lower revenue

This highlights a key limitation of the analysis:

- The evaluation focuses on risk (defaults)

- It does not directly account for profitability

To fully align with business objectives, we need to extend the analysis to include:

- Net Present Value (NPV)

- or profit per approved loan

This would allow decision-makers to evaluate:

The trade-off between risk reduction and business growth

Final Takeaway

There is no universally “best” policy — only a best policy given the company’s risk appetite.

- If the priority is minimising losses → Policy A

- If the priority is maximising growth and scale → Policy B

The optimal strategy likely lies in balancing both.

5.

Resources

Below you can find a PDF of the analysis that was done for the project using R.